Where Does My Money Go Every Month? Find Out in Minutes

Your money goes to a mix of fixed bills and small, frequent purchases that are easy to forget. The fastest way to see the full picture is a three-month statement review: download every bank and card PDF, group spending into fixed versus discretionary categories, and list the top merchants. That turns guesswork into a clear monthly spending breakdown.

Why mental tracking fails

Paychecks feel large. Coffee, delivery, rides, and one-click orders feel small. Your brain remembers the rent check and forgets the twenty tiny charges that add up to the same size by month's end.

That is not a discipline problem. It is how attention works. A spending tracker exists because memory is a terrible ledger. If you only glance at your checking balance, you see the leftover—not the story of where the rest went.

Credit cards make the fog thicker. You spend now and feel the hit later, often split across multiple cards with different due dates. By the time the statement arrives, the “why” behind each charge has already faded. Asking “where does my money go every month?” is usually a request for a map, not another pep talk.

The three-month statement review method

Pick a quiet hour and pull statements for the last three full months—every checking account and every credit card you use. Three months smooths out one weird vacation week or one big annual bill without turning the project into a year-long archaeology dig.

- Export PDFs from each issuer (or download CSVs if that is easier for you).

- Work month by month so seasonality stays visible—January heating costs and July travel should not blur into one average.

- Ignore transfers between your own accounts; they move money, they do not spend it.

- Write down category totals and the top five merchants per month.

- Note one surprise per month. That list becomes your action plan.

You do not need perfect bookkeeping software on day one. You need an honest map. A bank statement analyzer or a careful spreadsheet both get you there; the point is looking at real transactions, not guessing from memory or from a single account balance.

Group spending so the picture makes sense

Start with two buckets, then refine. Fixed costs are the floor. Discretionary costs are where most people find room to change course.

- Fixed: rent or mortgage, utilities, insurance, minimum debt payments, tuition—costs that barely change month to month.

- Discretionary: dining, shopping, entertainment, travel, hobbies—costs you can cut or reshape without rewriting your life overnight.

Inside discretionary, use simple category clusters: groceries, food delivery, subscriptions, transport, personal care, misc. Keep the list short. Ten categories you will actually use beat forty you will abandon after week one.

When the same merchant shows up under two names, merge them. Issuer labels are messy; your categories should not be. A useful expense tracker view is one you can explain out loud in thirty seconds.

Name the leaks

Most people who ask this question already know about rent. The surprise is almost always one of these quieter drains:

- Subscriptions you forgot to cancel, stacked free trials that converted, or “only $8” services that add up across a household.

- Delivery and takeout that never feels like a meal plan but behaves like one when you total the month.

- Fees—late fees, overdraft, ATM, foreign transaction—quiet lines that rarely get a category of their own.

- Duplicate merchants across cards (same store, two payment methods) that look small in each portal and large combined.

Write the leak names down. Naming them is the first step toward changing them. A budget planner works better when it starts from real leaks, not from a generic percentage template you found in a blog post.

Make it a monthly ritual, not a spreadsheet weekend

The three-month deep dive teaches you the shape of your spending. After that, switch to a lighter monthly review: one statement cycle, same categories, same top-merchant check. Fifteen focused minutes beat a quarterly panic session that you keep postponing.

Put it on the calendar the day after statements usually post. Treat it like taking out the trash—regular, boring, done. The goal is not a perfect spreadsheet. The goal is an answer you trust when someone asks where the money went.

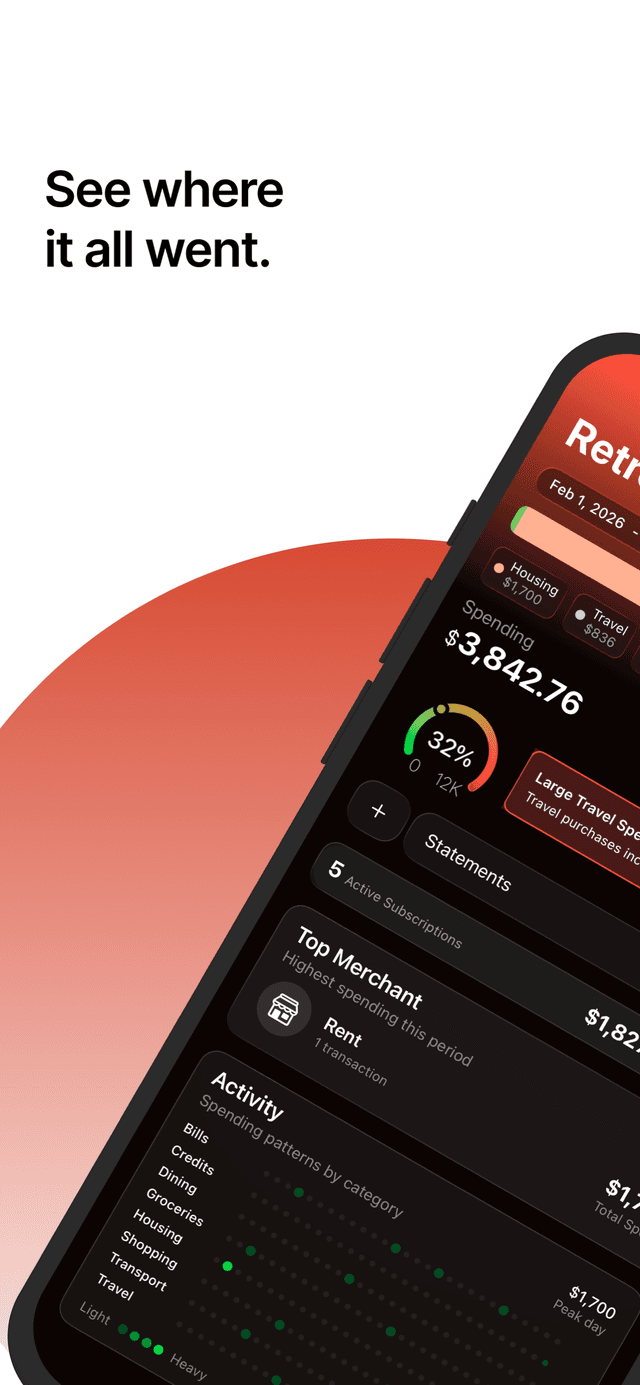

If you want that review without building the sheet yourself, upload each PDF to RetroBudget. The AI expense tracker categorizes every transaction and shows a spending breakdown by category, merchant, and card—so the question gets an answer in minutes, not a weekend.

Do it with RetroBudget

- 1

Get RetroBudget free on the App Store

Install the free iPhone app. No bank linking and no setup wizard—just a private money manager ready for statements.

- 2

Upload a PDF bank or credit card statement

Export last month’s statement and upload it. Live Activity tracks processing while AI categorizes each line.

- 3

See where it all went

Open the spending breakdown by category, merchant, and card. Spot the totals that surprise you first.

- 4

Repeat each month

Upload the next statement when it arrives. Turn the big question into a short monthly ritual instead of a once-a-year audit.

Quick answers

How far back should I look to see where my money goes?

Three full months is a strong default. One month can be a fluke; a full year is thorough but slow. Start with three, then keep a lighter monthly review going.

Should I include cash spending?

Yes, if cash is a real part of your month. Add a simple cash estimate or log withdrawals as a category so ATM pulls do not look like mystery spending.

What if I have multiple cards and accounts?

Gather every statement for the same calendar month. Review them together so you do not miss spending that left one card while your checking balance looked fine.

Can RetroBudget answer this without linking my bank?

Yes. Upload PDF statements you already have. RetroBudget categorizes transactions with AI, shows the breakdown, and deletes the statements after processing—no bank login required.