How to Analyze a Bank Statement to See Where Your Money Goes

To analyze a bank statement, download the PDF, scan every line for recurring charges and fees, group spending into categories, then split fixed costs from discretionary ones. A short monthly ritual — totals, top merchants, one surprise — shows where your money goes without needing a live bank connection.

What to look for line by line

Open the statement and treat it like a receipt for the whole month. Do not jump straight to the ending balance. Walk the transaction list with a few questions in mind.

- Recurring charges — Same merchant, same or similar amount, every month: streaming, cloud storage, gym, insurance add-ons, app trials that never ended.

- Fees — ATM fees, overdraft, foreign transaction, late payment, paper-statement fees. Small lines that add up when you ignore them.

- Spending clusters — Three food-delivery orders in a week, a burst of online shopping after payday, gas fills that jumped when you drove more. Clusters explain lifestyle better than a single big purchase.

- Transfers and cash — Transfers to savings or another person are not "spending" in the same sense as a store purchase. Tag them so they do not distort your categories.

Fixed vs discretionary: a useful split

After you have categories, sort them into two buckets. Fixed (or near-fixed): rent or mortgage, utilities, insurance, minimum debt payments, transit passes. Discretionary: dining out, shopping, entertainment, travel, hobbies.

You cannot cut rent overnight. You can usually change discretionary totals within a month. Knowing the split keeps a bank statement analyzer exercise honest — if 70% is fixed, the leverage for next month lives in the other 30%, not in guilt about every grocery run.

A common starter category set: Housing, Utilities, Groceries, Dining, Transport, Subscriptions, Shopping, Health, Travel, Income, Transfers, Other. Adjust names to how you actually live. Consistency month to month matters more than perfect labels.

A monthly review ritual that takes minutes

Pick a recurring date after statements post. Same steps every time:

- Download the PDF (and any credit card PDFs you use).

- Total spending by category.

- List the top three merchants by amount.

- Write down one surprise — a fee, a duplicate subscription, a category that blew past last month.

- Choose one action for next month. One is enough.

That ritual turns a bank statement into a spending tracker habit. You do not need a 20-tab spreadsheet. You need a clear breakdown and a decision.

How categorization reveals patterns

Raw merchant names hide patterns. "SQ *COFFEE" and "TST*CAFE" look different until both sit under Dining. Categorize first, then judge. People often discover that "I barely eat out" is three delivery apps plus lunch near the office — same category, same wallet.

Do this for two or three months and trends show up: subscriptions creeping, seasonal travel, holiday shopping. That is the real payoff of analyzing statements — not a single pie chart, but a picture you trust enough to plan against.

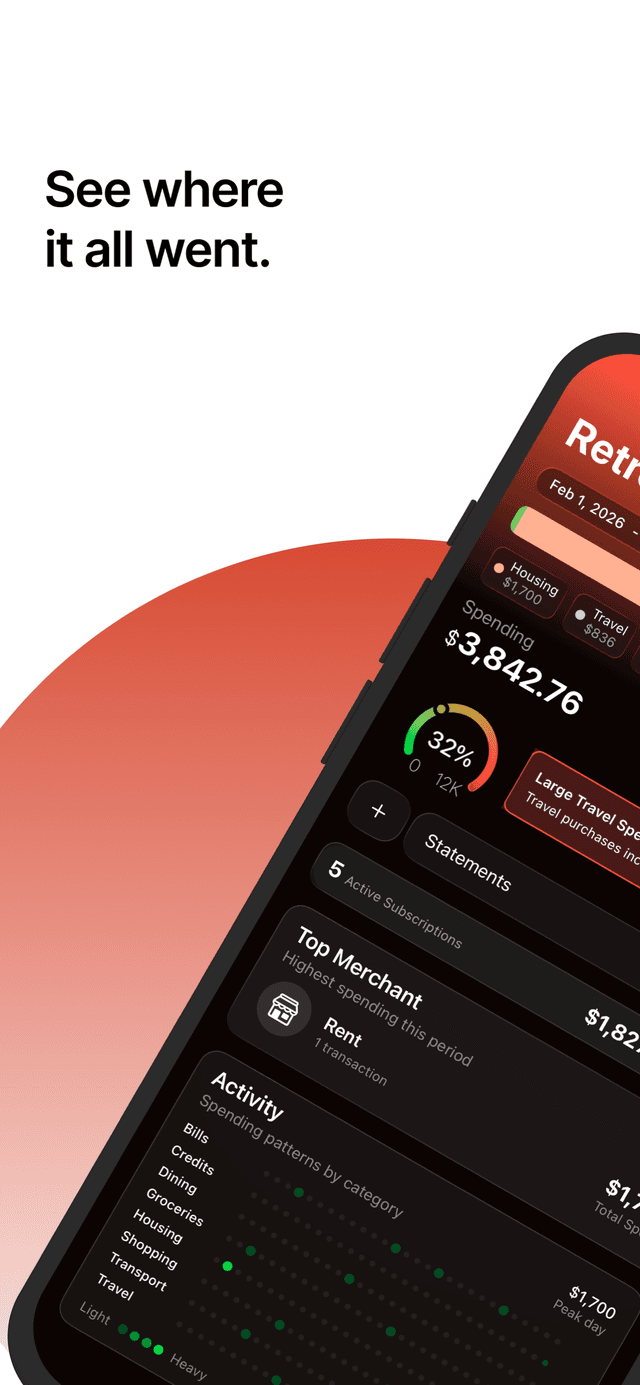

Do it with RetroBudget

- 1

Download RetroBudget

Install the free iPhone app from the App Store. No bank sync setup — you bring the statement.

- 2

Upload your PDF bank statement

Export last month's statement from your bank. Upload it. Live Activity tracks processing while AI categorizes each transaction.

- 3

Read the breakdown

Open the dashboard for totals, category gauges, and top merchants. Skim the ledger for fees and odd charges you would have missed in a quick glance.

- 4

Act on one pattern

Use bill and recurring-spending review to spot subscriptions, then set a simple next-month plan in the budget planner from what the statement actually showed.

Quick answers

How long should analyzing a bank statement take?

With a categorized breakdown, a focused review can take 10–20 minutes. Line-by-line in a spreadsheet takes longer. The goal is a clear spending picture and one decision, not a perfect audit.

Should I use the PDF or the bank's app transactions list?

The PDF is usually the most complete official record for the statement period. App feeds are handy day to day, but the monthly PDF is ideal for a full review and for any tool that analyzes bank statements offline.

What if I have both a checking account and credit cards?

Analyze each statement, then combine the story. Credit cards often hold most discretionary spend; the bank statement catches transfers, fees, and debit purchases. RetroBudget supports multi-card tracking so you can review them together.

Do I need to categorize every tiny purchase?

Aim for useful buckets, not perfection. A $3 coffee can roll into Dining. Focus energy on large lines, recurring charges, and categories that drive next month's plan.