How to Track Spending Across Multiple Credit Cards

To track spending across multiple credit cards, review one calendar month at a time: download every card’s statement, put transactions on the same timeline, and normalize categories so issuer labels match. Watch for the same merchant on two cards. Then total by category and by card for a unified view.

Why multi-card spending fragments your picture

One card for points. One for the grocery store. A store card for a discount. A debit card for cash-like purchases. Each issuer shows a clean mini-story. Together they hide the real month.

Statement cycles rarely align. Category names differ—“Merchandise” on one PDF, “Shopping” on another. Issuer apps optimize for that card's rewards, not for your household budget planner. If you only open one portal, you systematically undercount the rest.

Per-card reward dashboards make the problem worse. They celebrate category bonuses on Card A while Card B quietly carries the dining you forgot about. Multi-card tracking is not about collecting more apps. It is about assembling one picture from every statement you already receive.

Assemble one calendar month, not one statement cycle

Pick a calendar month—March 1 through March 31, for example—and gather every credit and debit card statement that covers those dates. You may need two PDFs per card when cycles overlap the month boundary. That is normal and worth the few extra downloads.

- List every card you spent on, including store cards and digital cards you barely think about.

- Download each PDF (or CSV) for the overlapping cycles.

- Filter or highlight only transactions that posted in your chosen month.

- Exclude payments to the card itself; those are balance movements, not spending.

- Keep refunds visible so a return does not look like mystery income in your notes.

Working in calendar months makes rent, paycheck timing, and “how did April feel?” line up with how you actually think about money. Issuer cycles are for the bank. Calendar months are for you.

If you share expenses with a partner, agree on the same month window before you start. Comparing your Card A March to their Card B mid-cycle dates is how double-counting and gaps both sneak in.

Normalize categories and catch merchant overlap

Create one category list and force every issuer label into it. Groceries stay groceries whether the bank called it “Supermarkets” or “Food & drink.” Consistency matters more than matching the bank's taxonomy.

Then scan merchants across cards. The same coffee chain or delivery app on two cards is still one habit. People who track cards in isolation often “fix” a problem twice without noticing it is the same leak wearing two statement skins.

- Build a single top-merchant list for the whole month.

- Note which card carried each charge—useful for rewards and for staying under limits.

- Flag annual fees and interest so they do not hide inside “misc.”

- Separate “business” or reimbursable charges if you mix personal and work spend on one card.

When categories and merchants finally share one system, patterns jump out: which card eats groceries, which card eats impulse buys, and which “small” charge is actually a weekly ritual.

Run a monthly all-cards ritual

Once you have the method, keep it light: when the month ends, collect every statement, categorize with the same system, and write three numbers—total spend, top category, top merchant. That is enough to steer the next month without living in a spreadsheet.

Optional fourth number: spend by card. Knowing that Card B carried sixty percent of dining is often more actionable than knowing dining was high in the abstract. You can change which card you pull out, or change the habit—either way starts with a clear split.

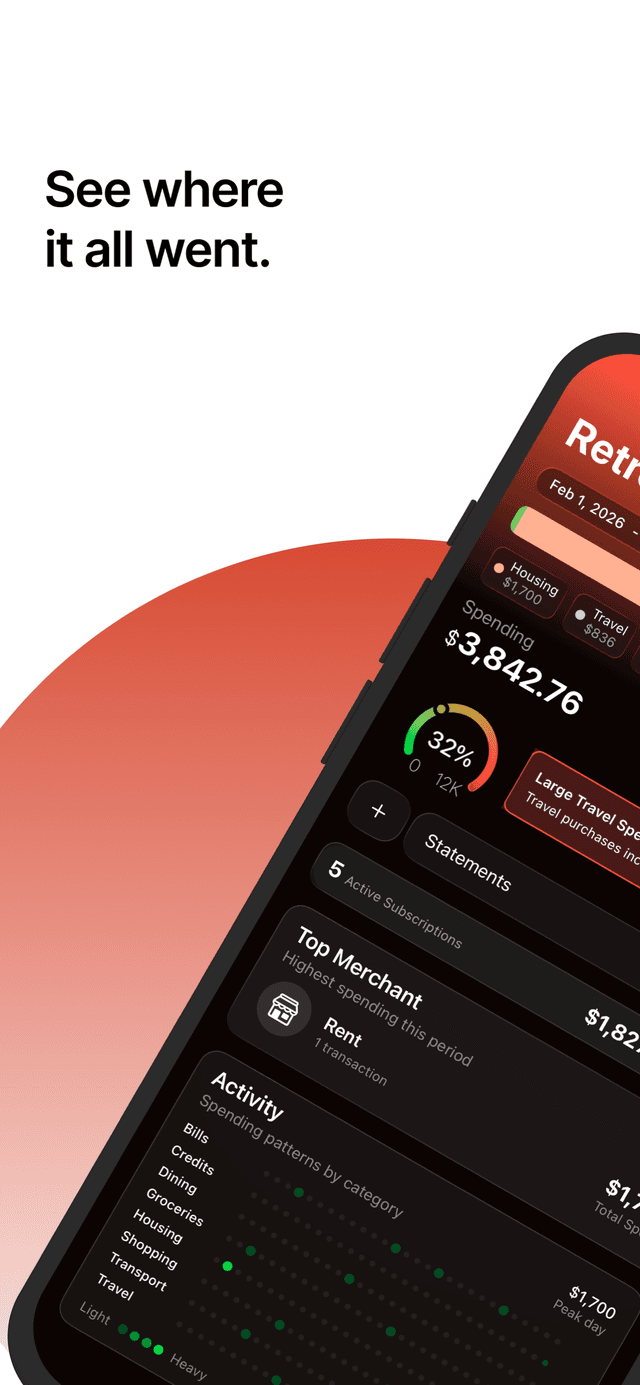

RetroBudget is built for this ritual. Upload each card's PDF statement; AI applies one consistent category system across issuers. You get a spending breakdown by card and a merged view by category and merchant—so multi-card tracking stops meaning five browser tabs and a weekend of cleanup. No account linking, no bank login; statements are processed, then deleted.

Do it with RetroBudget

- 1

Get RetroBudget free on the App Store

Install RetroBudget: AI Spend Tracker. Multi-card tracking is part of the workflow—no separate aggregator per issuer.

- 2

Upload each card’s PDF statement

Export statements from every credit and debit card you use, then upload them one by one. Live Activity shows while each file is processed.

- 3

Review one consistent category system

AI categorizes transactions across cards with the same labels. Compare the breakdown by card, then switch to merged category and merchant totals.

- 4

Make it your monthly all-cards review

When the next cycle closes, upload the new PDFs. Keep the same ritual so multi-card spending stays visible without bank linking.

Quick answers

Should I track credit cards and debit cards together?

Yes, if you spend on both. A complete expense tracker view needs every payment method for the same month. Otherwise debit grocery runs disappear while credit dining looks like the whole story.

What if my card statement cycles do not match the calendar month?

Download the overlapping statements and keep only transactions that fall inside your chosen month. Calendar months are easier to compare to income and bills than issuer cycles.

How does RetroBudget handle multiple cards?

Upload a PDF for each card. RetroBudget categorizes transactions with one AI category system and lets you review spending by card as well as by category and merchant. No account linking required.

Do I need to connect each card through a bank aggregator?

Not with a statement-based approach. Export PDFs from each issuer and upload them. RetroBudget never asks for card or bank login credentials.